There’s A Better Way To Earn Interest From Banks And It’s Not Your Savings Account

We’re all looking at ways to improve gains without doing much with our money — that’s why we trust in the magic of compound interest. The problem is, you hardly see banks offering interest rates at 1.00% anymore. Bank Of America, Chase, Wells Fargo, HSBC all offer .01% on regular savings accounts. That’s right, a measly .01% — if you were to put in $100 a month ($1,300 with initial deposit of $200), you’d end up with — you guessed it — $1,300.08. You made .08 cents on interest! That’s awful. You need to find out a way to get better returns than that.

There is one — of many — things you can do that can improve the amount of money you can get from banks. It’s called CD laddering.

A certificate of deposits basically allows your money to grow without much risk involved. These are high-grade government-insured deposits of which banks give you higher interest than what you’d normally receive from their regular savings accounts. With CD laddering, you’re using time and interest to your advantage.

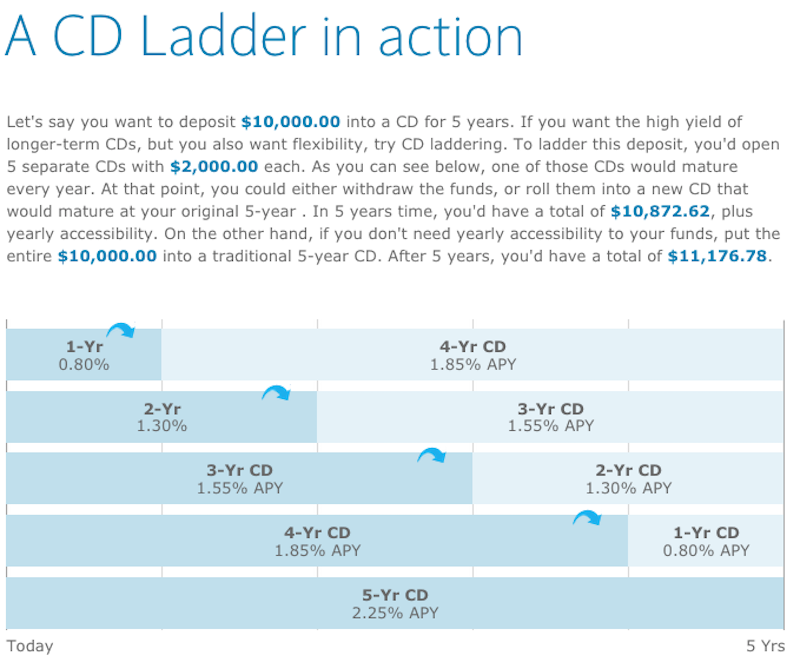

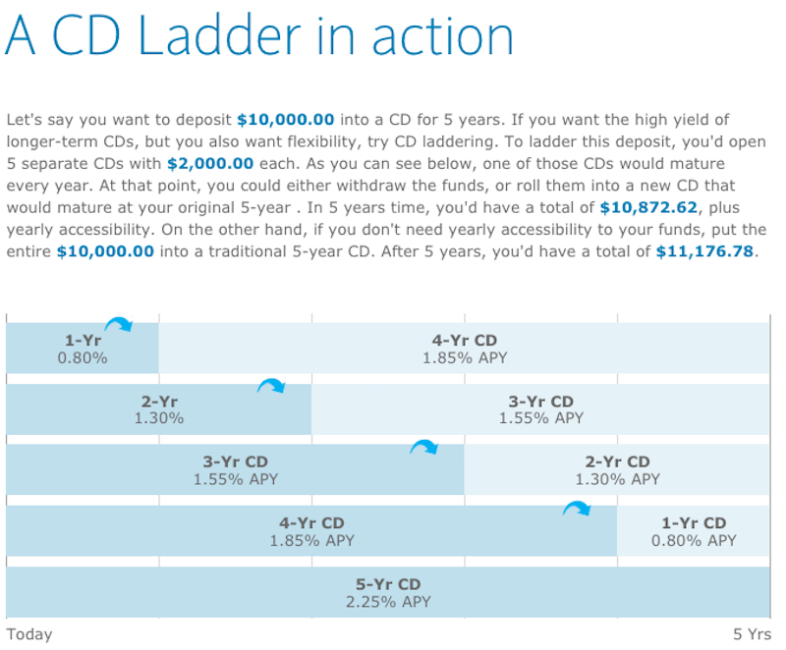

Think about it like this. You have $10,000 to invest. Putting that in a savings account means you’d get anywhere from .01 to 1.0%. In five years time, you’d get $10,005.00 to $10,512.49, respectively. With CD Laddering, however, you’d split the money up evenly five ways (or whatever you think is best) to take advantage of being both flexible (in case rates go up) and the high yield of long-term CDs (what you have now). Here it is in action:

In five years time, you’d have $11,176.78, which is $664.29 more than what you’d get from having your money in a 1.0% savings account, and $1,171.78 more than .01% account. Cool, right?

Of course, when the Fed decides it’s time to increase rates, that’s when you’d see your long-term CD lose out on the potential gains (you’re locked into the interest rate once you hand the money over until it matures). But that’s why you put some of your money into 1-year and 2-year CDs. You smart person, you! ![]()