I Didn’t Know Jack Sh*t About Finance, So I Tried To Do Something About It

I’ll cut right to the chase.

I started with zero knowledge in finance. Actually, if I can be candid for just a moment, I’d like to say I still don’t. I was never going to be a finance major — at least, that’s what I thought in college. In fact, the only class I took that dealt with how the financial world worked was my macroeconomics class, which I passed with a C+.

My birthday was yesterday (I’m an Aries, baby!), which means I’m one year older, and one step closer to completely breaking down and wondering what it is I’m supposed to be doing in life. (I read James Altucher’s Are You The Exception Or The Rule just a moment ago, and I’m fairly certain the answer is, “Nothing. Because there are no rules.” But, I will add, what I think I’m supposed to be doing is amassing wealth, developing ways to get ahead of the curve, build networks, destroy enemies, play a lot of cool video games, watch some fun shows, eat good food, and so on and so on.)

A couple of years ago, I stumbled my way into a financial technology meetup. Seasoned investors went around the room introducing themselves. Then, as it goes, it was my turn. (And I did my absolute best to avoid meetups and events that did this roundabout introduction.)

“Hi, I’m Michael…” (this is when my face turned red) “…and I’m a freelance writer for a tech blog.”

The room chuckled.

“What are you doing here?” one of the panelists asked.

Oh boy.

“I-I just wanted to get to know the industry better,” I stammered.

That was a good answer. The room murmured in approval.

“Good to see you here, Michael,” the host said. “Hope you get something out of it.” His name was Jon.

You see, I only went to this because I saw that someone was there from Bain Capital — the very same LLC that Mitt Romney co-founded.

“This sounds fun,” I remember telling a friend of mine.

“Make sure you ask about Mitt Romney,” my friend joked.

“What if, like, I ended up working for Bain?”

“Then I’d say you’re an evil person.”

I did tech write-ups for about almost two years, learned a heaping amount about how tech companies work, what legacy languages were, got to see some sweet startups give pitches (I actually saw Uber and Dwolla give pitches in front of investors — looking back on it, it’s really cool to see how far they’ve come), listened to some incredibly smart and passionate people talk about their work, and here I was, amidst these men and women listening to this man say he raised $600 million (all without batting an eye), at this financial tech meetup, wondering why the hell he was talking about insurance.

“There’s no scalability in insurance. They use lead generation, which is not a great business model. Insurance is heavily regulated and if you want to get into this space, you look to big data and data analytics…”

They served whiskey and chocolate in front of a huge window overlooking Bryant Park.

I stood by the window sipping whiskey, wondering if I, too, could be part of this world.

A man walked up to the window and peered down at the people ice skating in the park.

“What did you think of the talk?” he asked.

“I thought it was interesting,” I said.

He waved it off.

“Come on, don’t bullshit me. You said you’re a writer, right?”

I nodded.

“You write financial articles?”

“No… I, err, I write for a small tech blog. You know, I cover events that deal with startups.”

“Oh,” he said.

That was the extent of our conversation. That’s usually how it would go. “Oh,” and they’d shut up. That made me feel insignificant.

I have both The Intelligent Investor and Common Sense On Mutual Funds on my Kindle right now. I read maybe 1/3rds of the former and just about half of the latter. I did manage to get my hands on Margin Of Safety (it’s supposedly a very difficult book to obtain), and I read a couple of the Rich Dad Poor Dad books, too.

Reading them did give me insight as to how I should act and react in the market, but I think I learned most from what I call my $100 mistake, which started in January of 2014. (I also began to read those books later in the year, so it definitely helped to make the mistake first and read the books, which in turned helped me frame it and understand it better.) That $100 mistake was the best mistake I made (but it took me just around a year to fully grasp). It made me — it helped me — realize that I’m not cut out to be a trader — I don’t have the patience or the guts to pull the trigger on stock.

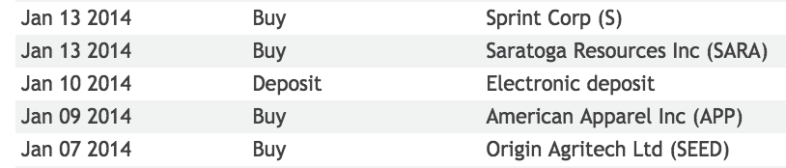

To be specific, I decided to put money into Sprint (when it was rumored that they were going to merge with T-Mobile) and American Apparel. I also bought this Chinese company that was supposedly the Chinese Monsanto and this small oil company operating in Upstate New York. Here’s the first thing I learned: Do your own research. Don’t buy because someone told you it’s a bargain (or that it’s undervalued and really “hot right now”). It’s terribly obvious, right? Do your own research. But I had entered the market without a mentor, no one had coached me what to do, what I should look for, what P/E and book value meant…

Anyway, Sprint fell from $9.38 to $4.25 (when I sold). American Apparel fell from $1.17 to $1.07 (I actually bought more shares when they were at $.65). I ended up selling Origin Agritech at $1.30 (I bought them at $2.60). I currently own shares of Saratoga Resources and Precision Drilling Corporation. Oil: go big or bust, baby! (Speaking of oil — I just really need to get this off my chest, because it’s been bothering me a lot — I’ve been tracking Helmerich And Payne since last November, just around when oil started to crash. You know people say to “buy low and sell high,” right? Well, in late January, HP (not Hewlett Packard, their ticker is HPQ) fell to $54.00. I read somewhere that they were going to drop to the high 40s, so I held out, but they’re in the $70s now, and I feel like a dumbass for not going through with the purchase. Which, again, is a testament to just how risk averse and, as Tversky and Kahneman, would say, demonstrates loss aversion to a tee. Okay, and greed. I’m fucking greedy.)

Yeah, so all-in-all, coupled with the brokerage fees and the losing streak, I decided that trading stock was not something I’m good at, and decided to read up on what and how to invest. For people who aren’t particularly interested (or have no idea what to invest in, what to look for, what to read, what the fuck their quarterly reports mean), then you’d probably want to put money into an index fund or ETFs. I know it’s wise to do your own research. It’s better you knowing what you’re getting into yourself, but with the incredible amount of information available and time you end up spending reading and trying to make heads and tails of the data presented to you, it’s really, really quite difficult.

Right now, I have money in a S&P 500 index fund and a Small-Cap index fund, both provided by Schwab. I’m planning to put some into a bond fund later — for “diversification” purposes, and hope to add an international fund some time this year, too.

There’s two more things that I’ve learned throughout this ordeal: “Stay your course,” as Jack Bogle said (you know, when you make your financial plan), and never speculate on the market. After all, Mr. Market is very fickle and cannot be trusted. Ever.

I think I’ve rambled on too much, like I’m apt to do when I’m thinking of doing something — but that isn’t a bad thing, right? ![]()